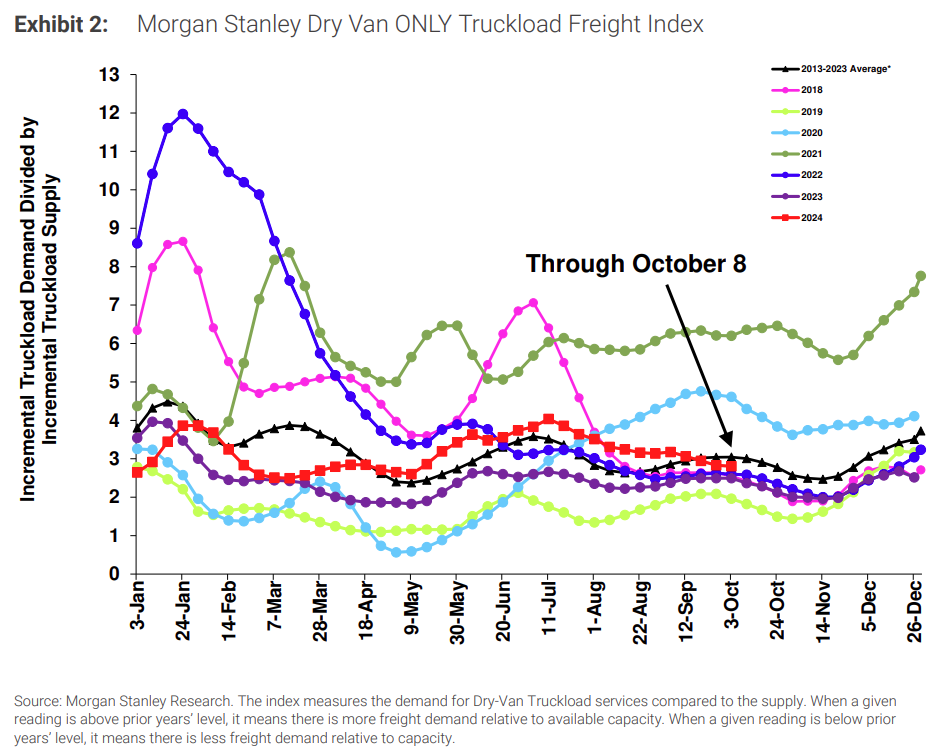

The Morgan Stanley Dry Van Freight Index is another measure of relative supply; the higher the index, the tighter the market conditions. The black line with triangle markers on the chart provides a great view of what directional trends would be in line with normal seasonality based on historical data dating back to 2007. Despite recent disruptions, the latest reading shows no meaningful activity or demand increase as of mid-October, with trends returning to the 10-year average amid seasonal cooling.

Morgan Stanley Dry Van Truckload Freight Index

Morgan Stanley Reefer and Flatbed Truckload Freight Indices

Morgan Stanley Reefer and Flatbed Truckload Freight Indices

The most recent ACT For-Hire Trucking Supply-Demand Balance Index reading ticked up to 56.9 from 51.1 in July, reflecting increased import levels and demand movement in late summer. The market continues to balance out. Slowing tractor sales and private fleet growth will continue to prime conditions for an inflationary flip, though it may not occur for several months.

ACT For-Hire Trucking Survey

ACT For-Hire Trucking Survey

In recent weeks, hurricanes and the port strike disrupted routing guides and caused a seasonal deviation. However, abundant capacity and limited spot market demand mitigated the impact of these events.

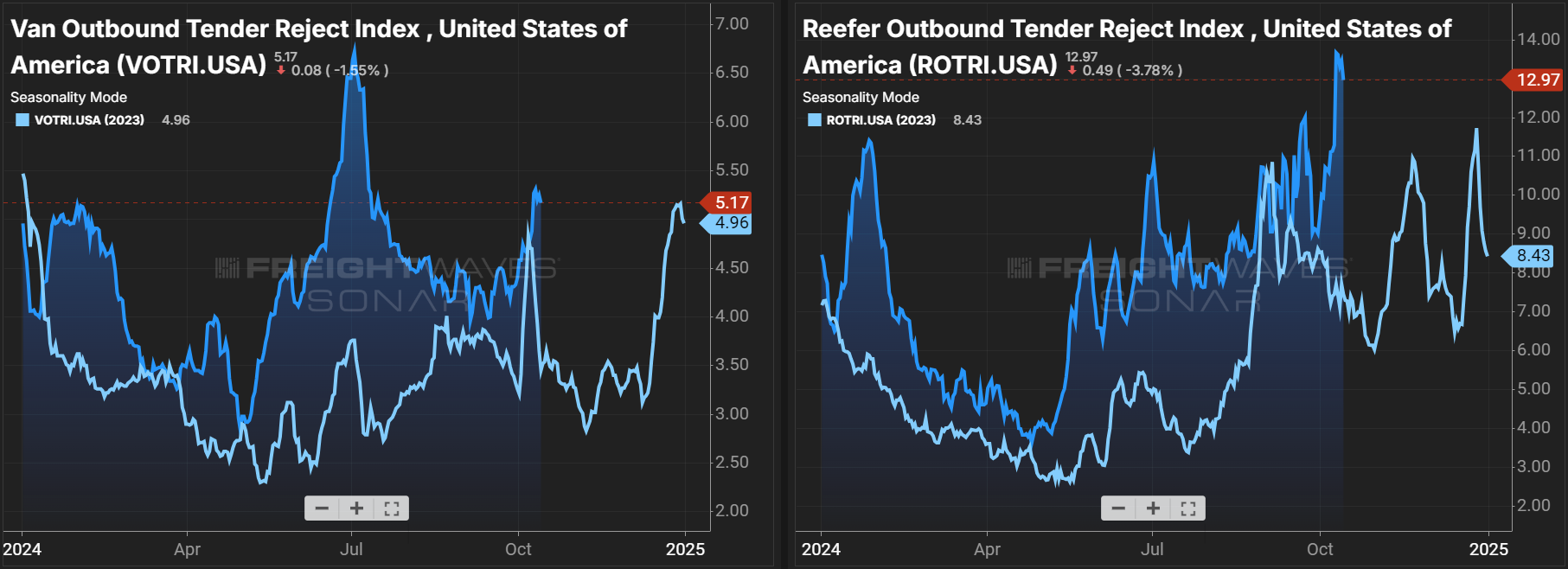

The Sonar Outbound Tender Reject Index (OTRI), which measures the rate at which carriers reject the freight they are contractually required to take, deviated slightly from 2023 trends. In October, demand typically eases, and capacity opens up. However, recent disruptive events caused regionalized volatility and a marginal increase in tender rejections at the national level. Conditions should continue to cool as November approaches, except for reefer markets, where tender rejections have reached the highest level in over two years.

Outbound Tender Reject Index (SONAR)

Outbound Tender Reject Index (SONAR)

Van & Reefer Outbound Tender Reject Indices

Van & Reefer Outbound Tender Reject Indices

The DAT Load-to-Truck Ratio measures the total number of loads relative to the total number of trucks posted on its spot board. The most recent reading shows three consecutive months of declines, confirming the market is cooling in line with seasonal expectations. Interestingly, rising rejection rates did not impact recent load-to-truck data, indicating that the spot market is not experiencing the pressure that typically comes with routing guide disruption.

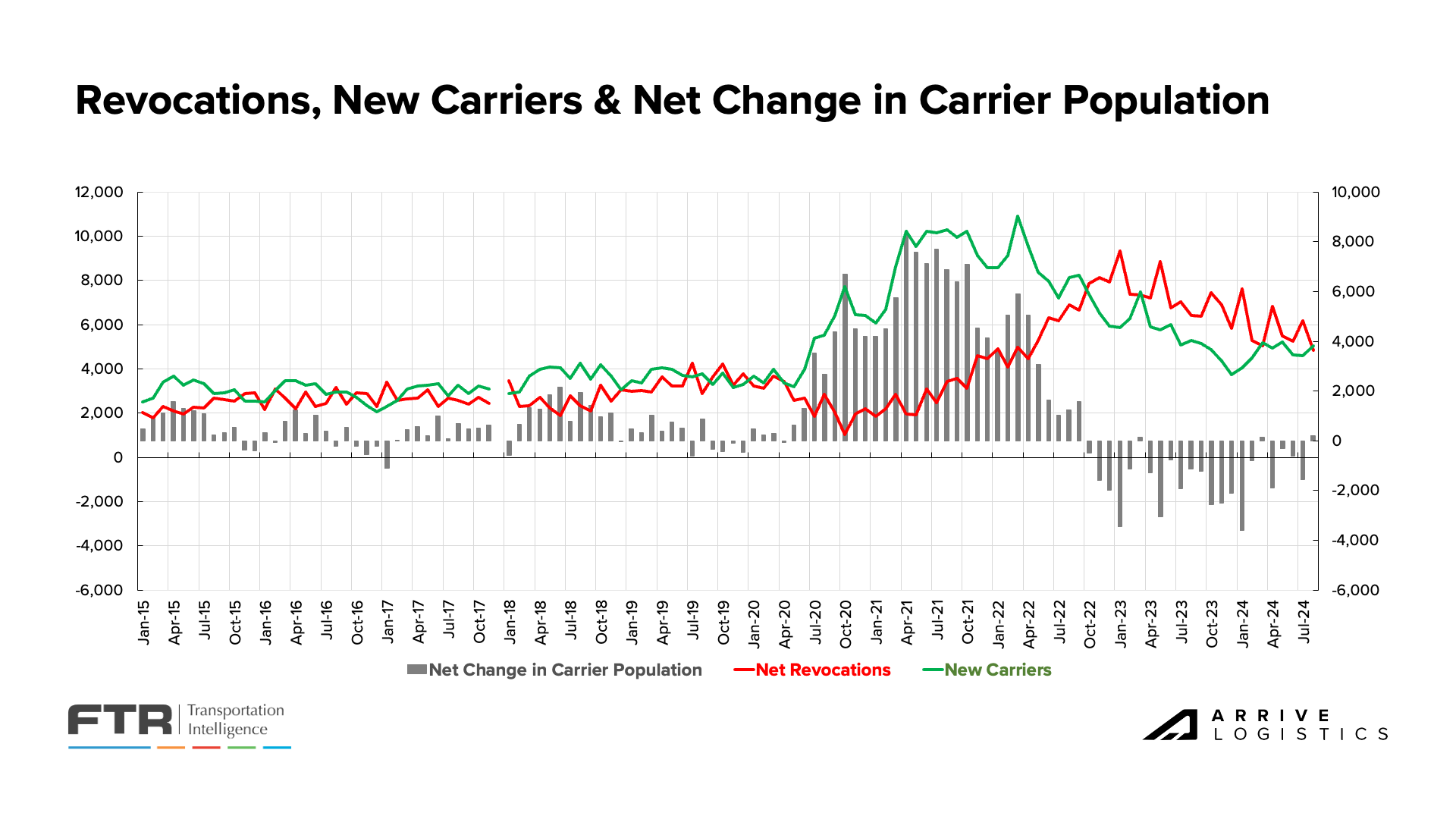

FTR’s latest revocation data shows a carrier population decrease for the 21st time in the last 24 months. Revocations ticked up month-over-month, while new entrants declined sequentially, indicating carriers continue to struggle or exit the market amid persistently low revenues. However, many may be holding out for a market inflection in early 2025.

FTR’s Carrier Revocations, New Carriers & Net Change in Carrier Population

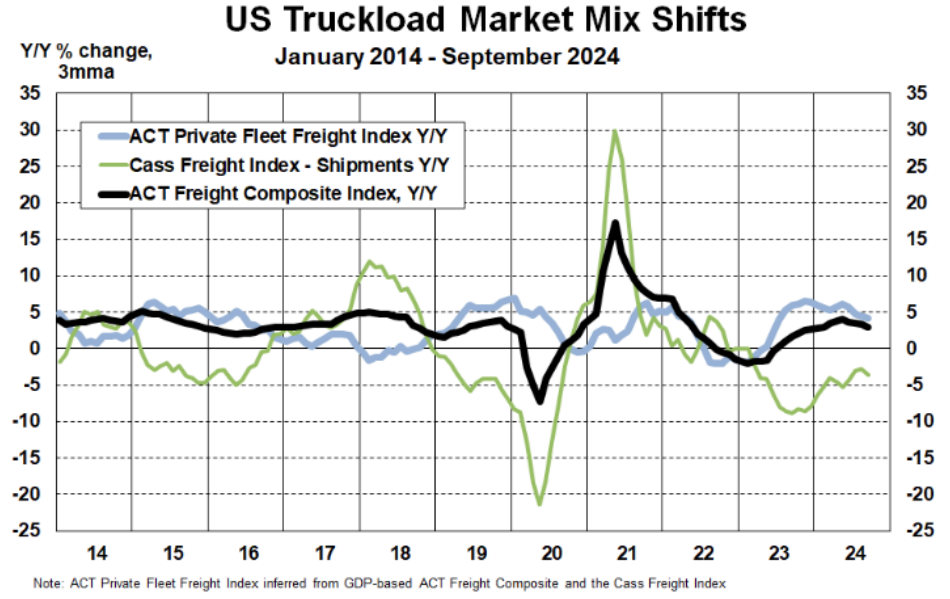

We continue to monitor the evolving role of private fleets as they increase their share of for-hire freight annually despite year-over-year shipment volume declines. With less freight available, for-hire carriers must negotiate aggressively on rates to maintain volume and revenue, which applies downward pressure on the market. If this trend continues and private fleet participation in the for-hire market grows, it could extend the current rate and supply environment.

US Truckload Market Mix Shifts, ACT Research & Cass Freight Index

US Truckload Market Mix Shifts, ACT Research & Cass Freight Index

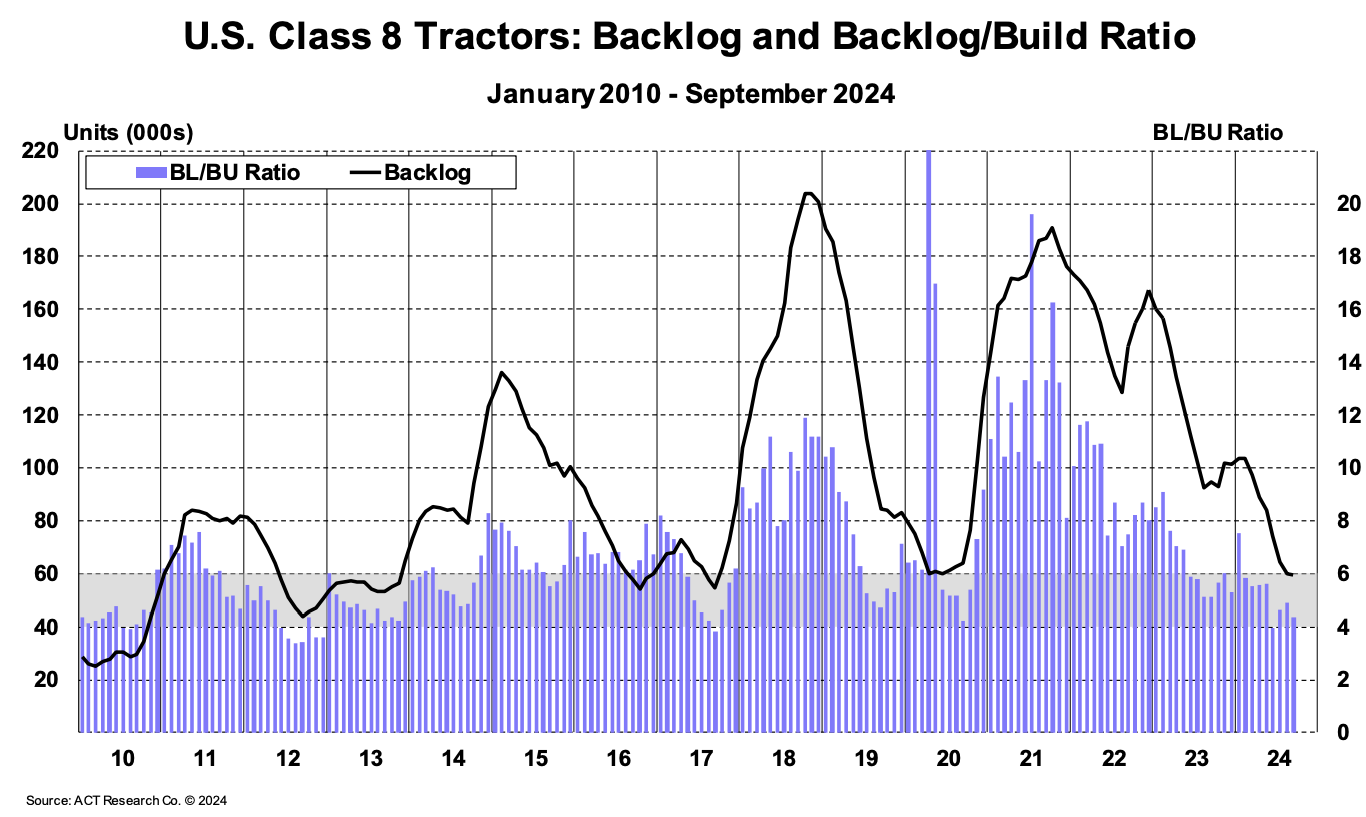

Based on the latest ACT Research data for U.S. Class 8 Tractors, the backlog-to-build (BL/BU) ratio fell from 4.9 months in August to 4.3 months in September, indicating that lower order rates continue to shrink the backlog. Despite experts forecasting a slow order season, backlogs may start to tick up as the season begins.

ACT Research, U.S. Class 8 Tractors: Backlog and Backlog/Build Ratio

ACT Research, U.S. Class 8 Tractors: Backlog and Backlog/Build Ratio

The most recent ACT For-Hire Driver Availability Index reading rose from 53.1 in July to 55.4 in August. This marks 27 consecutive months with a reading at or above 50 and indicates that there is no driver shortage. High driver availability likely correlates to older drivers staying active longer to cover higher living costs, as well increasing migration. Ultimately, the driver environment remains soft and is unlikely to change meaningfully in the near future.

ACT For-Hire Trucking Index: Driver Availability

ACT For-Hire Trucking Index: Driver Availability

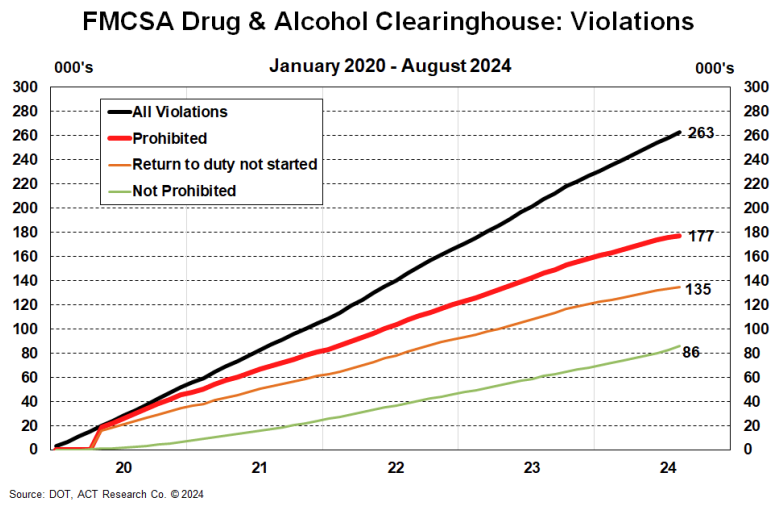

One of the more notable impacts on the capacity environment could occur on November 18th, 2024, when drivers with prohibited status will become ineligible for employment by law. According to ACT Research, approximately 177,000 drivers currently have prohibited status. Though many are already unemployed, these drivers have all been eligible for employment until now. Removing this population from the workforce amid holiday peak season volatility could create significant disruption.

Trucking jobs fell by 700 on a seasonally adjusted basis in September, a symptom of poor spot rate conditions and increased contract rate competition. Nearly 12,800 trucking jobs have disappeared since April 2024, including 4,400 in the past four months. The decline will likely continue as private fleet investment decelerates and carriers struggle to operate in the current rate environment. However, recent spot volatility plus the upcoming retail peak season could mitigate further job losses until early next year.

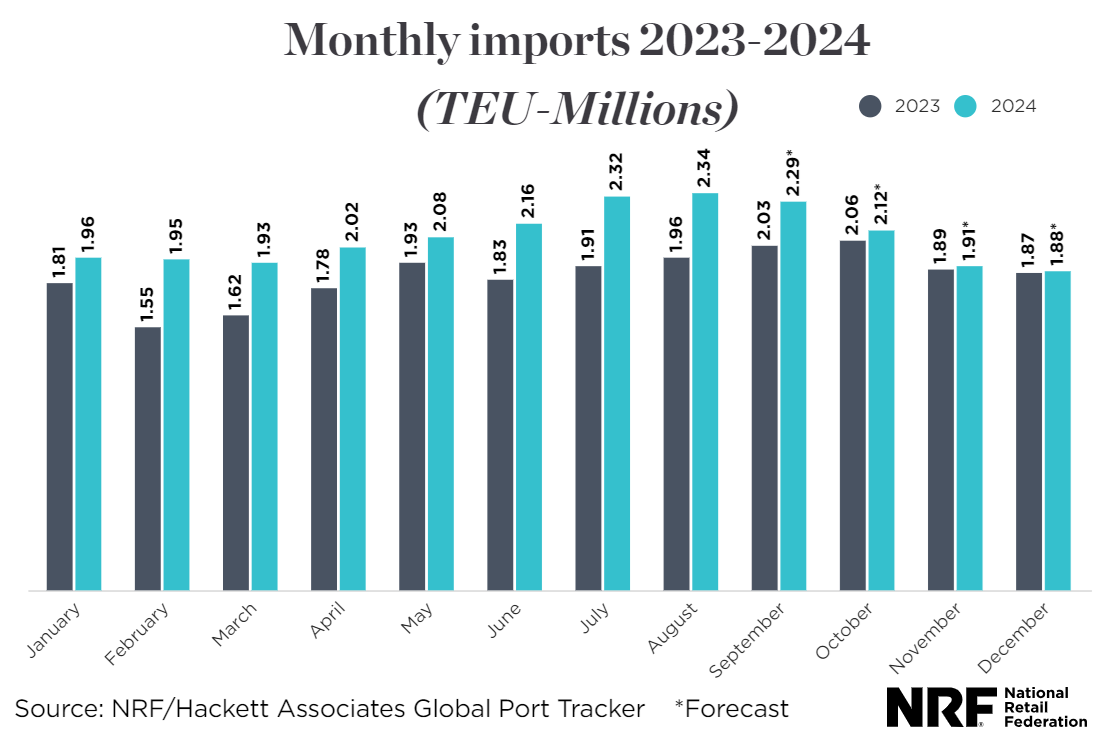

Forecasts continue to show stable freight volume. Both upside and downside risks are present, but there is no clear indication that demand shifts will impact the market in the near term. The latest National Retail Federation’s (NRF) forecast calls for year-over-year import volume increases for the remainder of 2024, with 25 million total TEUs expected by year-end.

While the East and Gulf Coast port strike is on hold until mid-January, shippers pushing freight forward during the summer months to avoid potential disruption led to a significant year-over-year increase in import volume. That surge has subsided, and imports for the rest of the year should be closer to 2023 levels than those from the first nine months of 2024. Despite the looming threat of the port strike resuming, major import forecast changes are unlikely for the remainder of the year as almost all holiday-related freight has arrived.

NRF Monthly Imports

NRF Monthly Imports

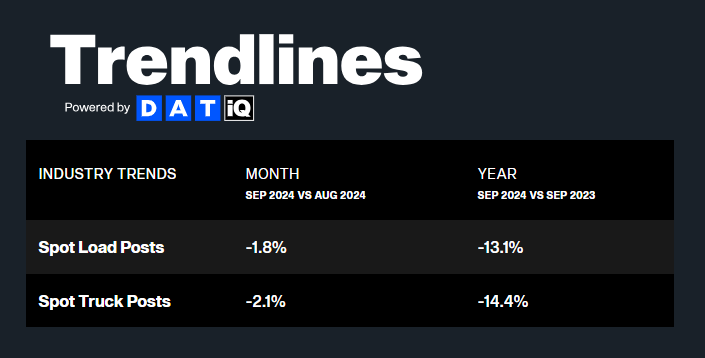

DAT reports that September spot load postings were down 1.8% month-over-month and nearly 13% year-over-year. The month-over-month decline mirrors August trends and indicates that the market may be cooling in line with seasonal expectations. The sequential freight reduction in September likely results from increased API utilization and fewer business days. Despite the pullback, this outcome is an improvement from the 12.3% month-over-month decline and 43.4% year-over-year decline in September 2023.

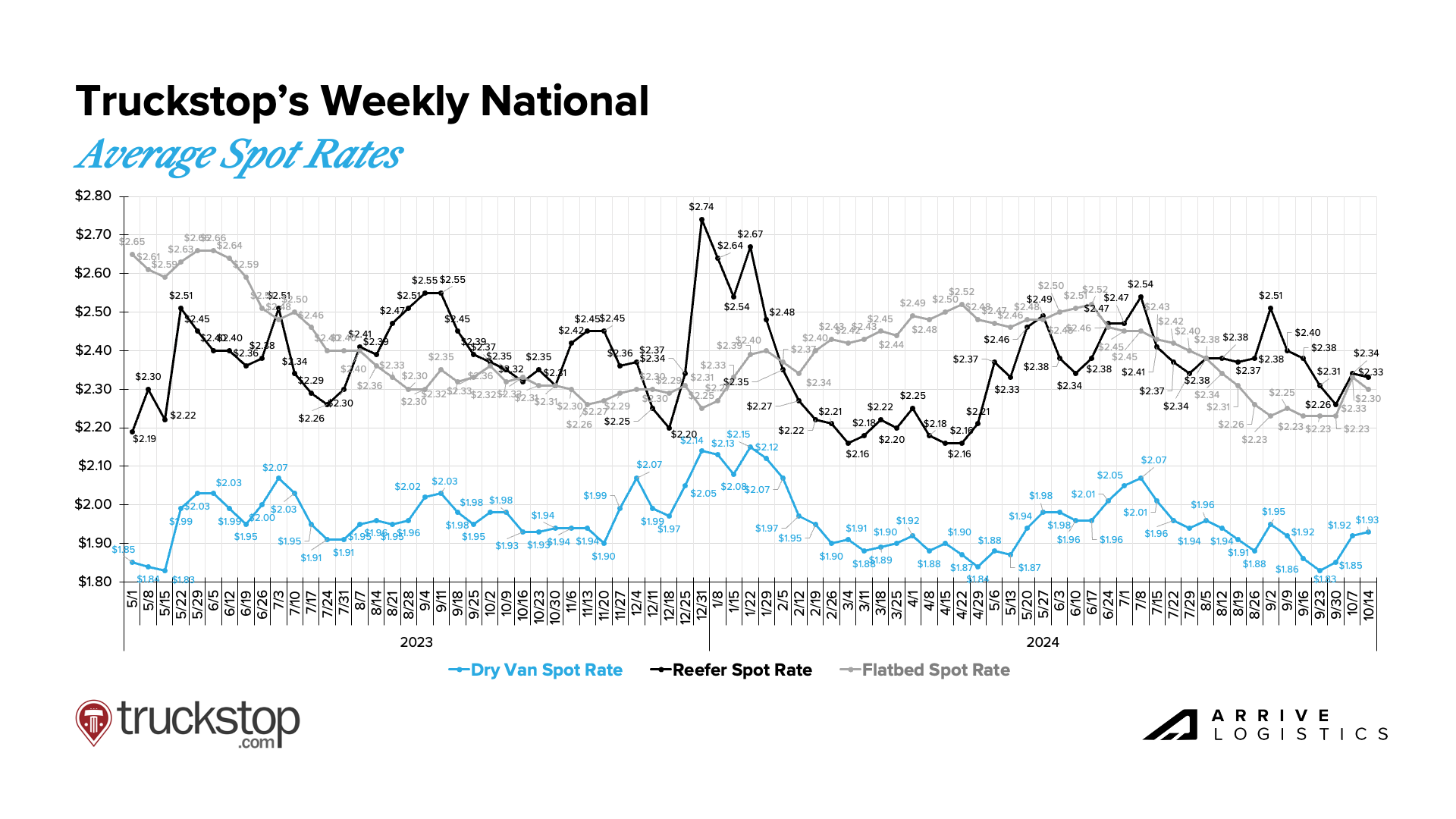

Recent disruptive events caused spot rates to rise sharply in late September and early October. These spikes coincided with increased tender rejections triggered by travel delays and road closures in affected areas. Most of that volatility has subsided and rates are expected to normalize during the second half of October and rise again as the holidays approach.

Truckstop Weekly National Spot Rate Average

Truckstop Weekly National Spot Rate Average

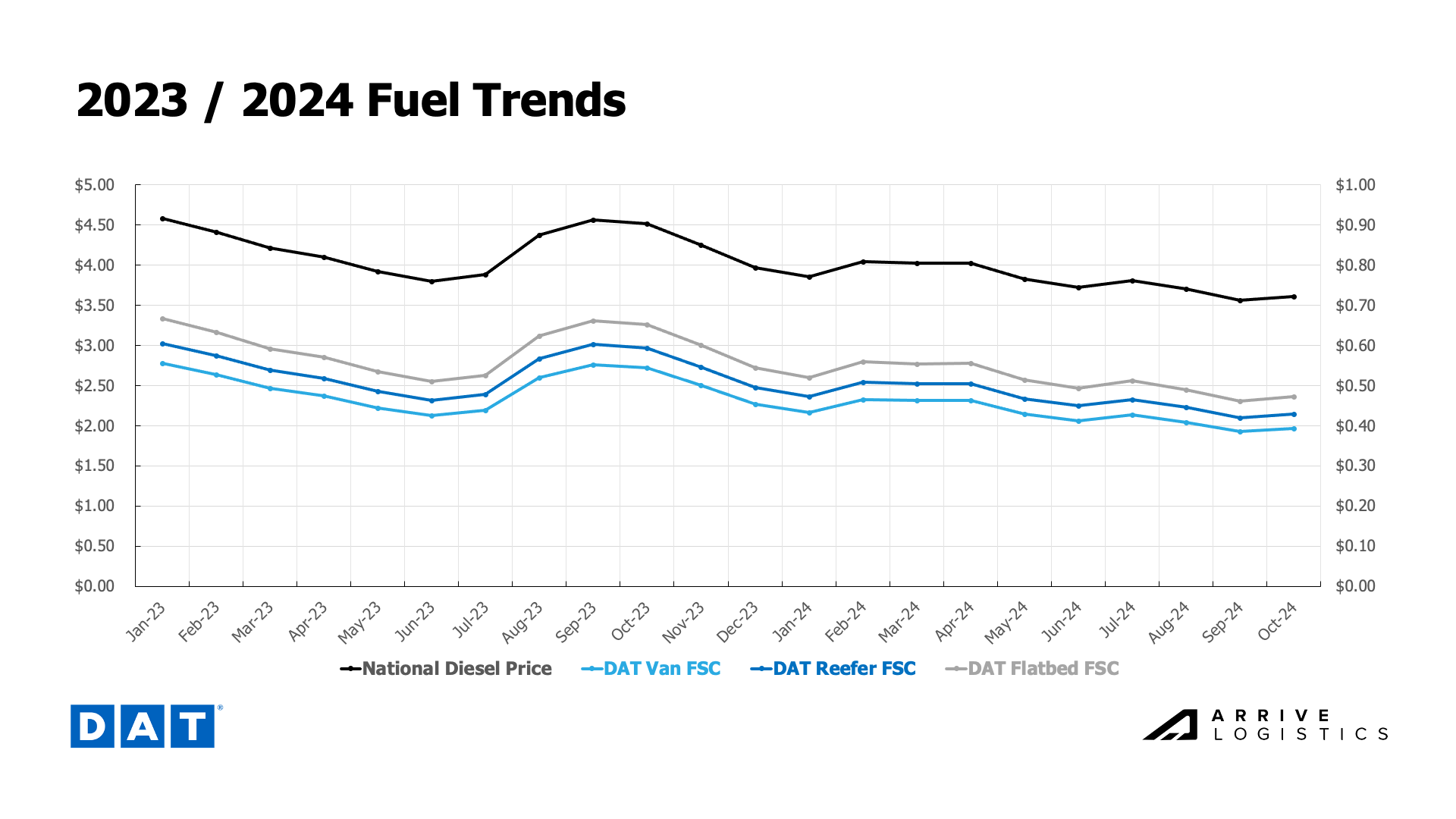

National diesel prices remain low but have ticked up in consecutive weeks, likely due to supply chain disruptions caused by Hurricanes Helene and Milton. Disruptions aside, fuel prices are steady, production remains strong and inventories are full. While current fuel prices should hold, winter weather and escalating conflicts in the Middle East remain risks.

DAT Fuel Trends

DAT Fuel Trends

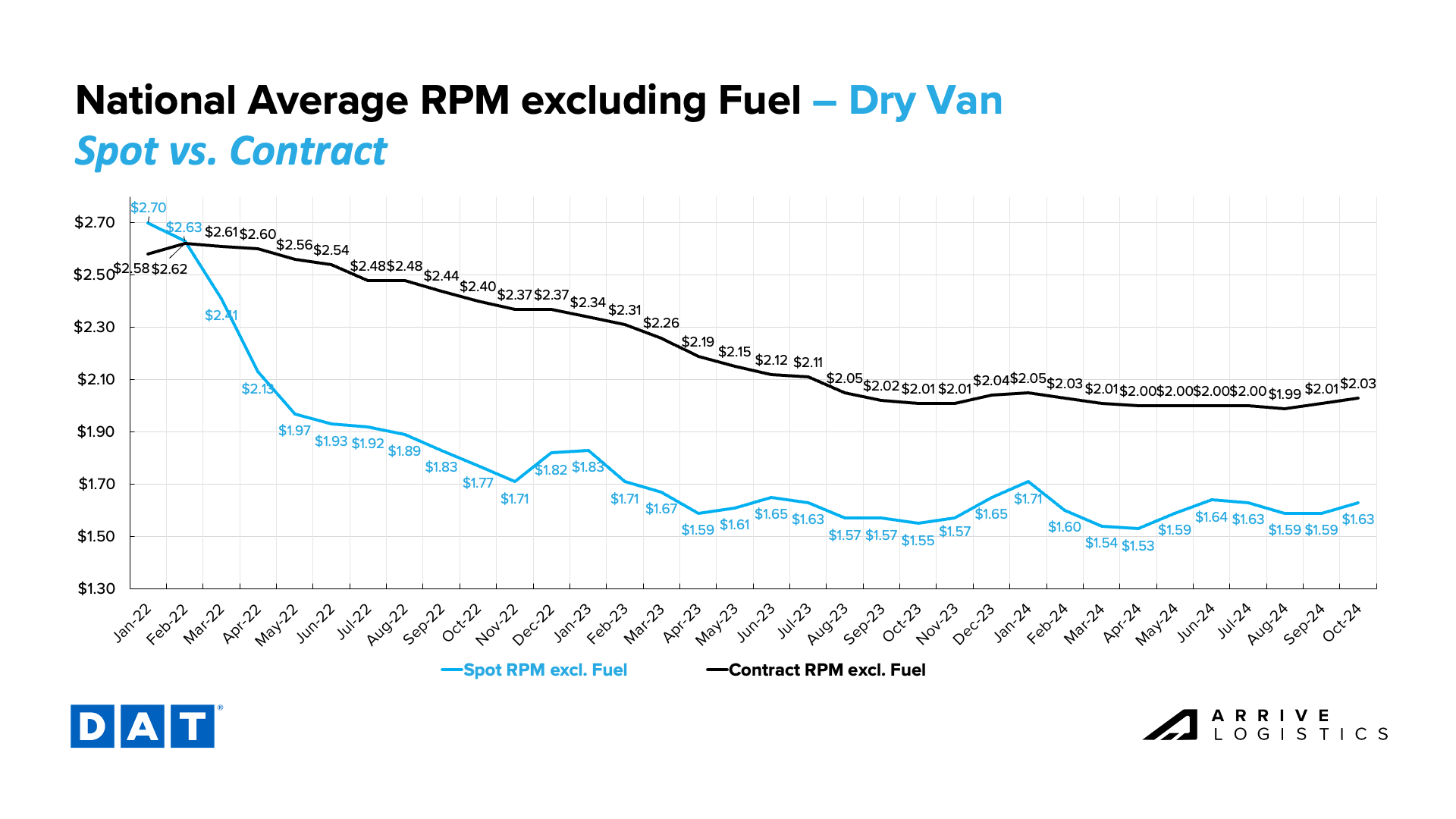

DAT dry van data shows spot rates were flat in September and then increased in early October, especially in regions impacted by Hurricane Helene and Milton. As conditions in those areas normalize, rates will likely return to levels observed in October 2022 and 2023.

Contract rates remain relatively flat, with marginal increases in September and early October. As the RFP season begins, shippers may look to lock in long-term contracts to insulate themselves against expected rate increases in 2025.

The spot-contract rate gap remains relatively wide at $0.40 per mile, excluding fuel, indicating the market is still safe from disruption.

DAT Dry Van National Average RPM Spot vs. Contract

DAT Dry Van National Average RPM Spot vs. Contract

Early October reefer trends differed slightly from dry van trends. Spot rates remain at $1.95 per mile, excluding fuel, and contract rates fell by $0.01 to $2.31 per mile.

This year’s spot rate trend is noticeably stronger than October 2022 and 2023, which had drops of $0.08 per mile and $0.06 per mile, respectively. Reefer market disruption should continue through year-end, causing rates to increase sharply.

DAT Temp Control National Average RPM Spot vs. Contract

DAT Temp Control National Average RPM Spot vs. Contract

Flatbed rates remain relatively steady but rose slightly in early October, likely due to increased recovery-related demand in regions impacted by Hurricanes Helene and Milton. Contract rates are still well above spot rates at $2.56 per mile.

DAT Flatbed National Average RPM Spot vs. Contract

DAT Flatbed National Average RPM Spot vs. Contract

Inflation continues to decline and move closer to the historical 2% target. The reading of 2.4% in September was the lowest since 2020. As a result, we expect more rate cuts in the near future, which would be inflationary and an upside risk to demand. As interest rates decline, consumer spending and housing activity should pick up and positively impact freight demand in 2025.

Recent Bank of America credit card data shows spending declined 0.9% year-over-year in September after rising 0.9% year-over-year in August. However, spending increased just 0.6% month-over-month on a seasonally adjusted basis as consumers remained cautious. Services sector spending increased on a quarterly basis, but retail spending continued to shrink slowly. Ultimately, consumer spending is expected to stay relatively stable until interest rates fall further and wages continue to grow.

Bank of America, Total Card Spending per Household

Bank of America, Total Card Spending per Household