"*" indicates required fields

"*" indicates required fields

"*" indicates required fields

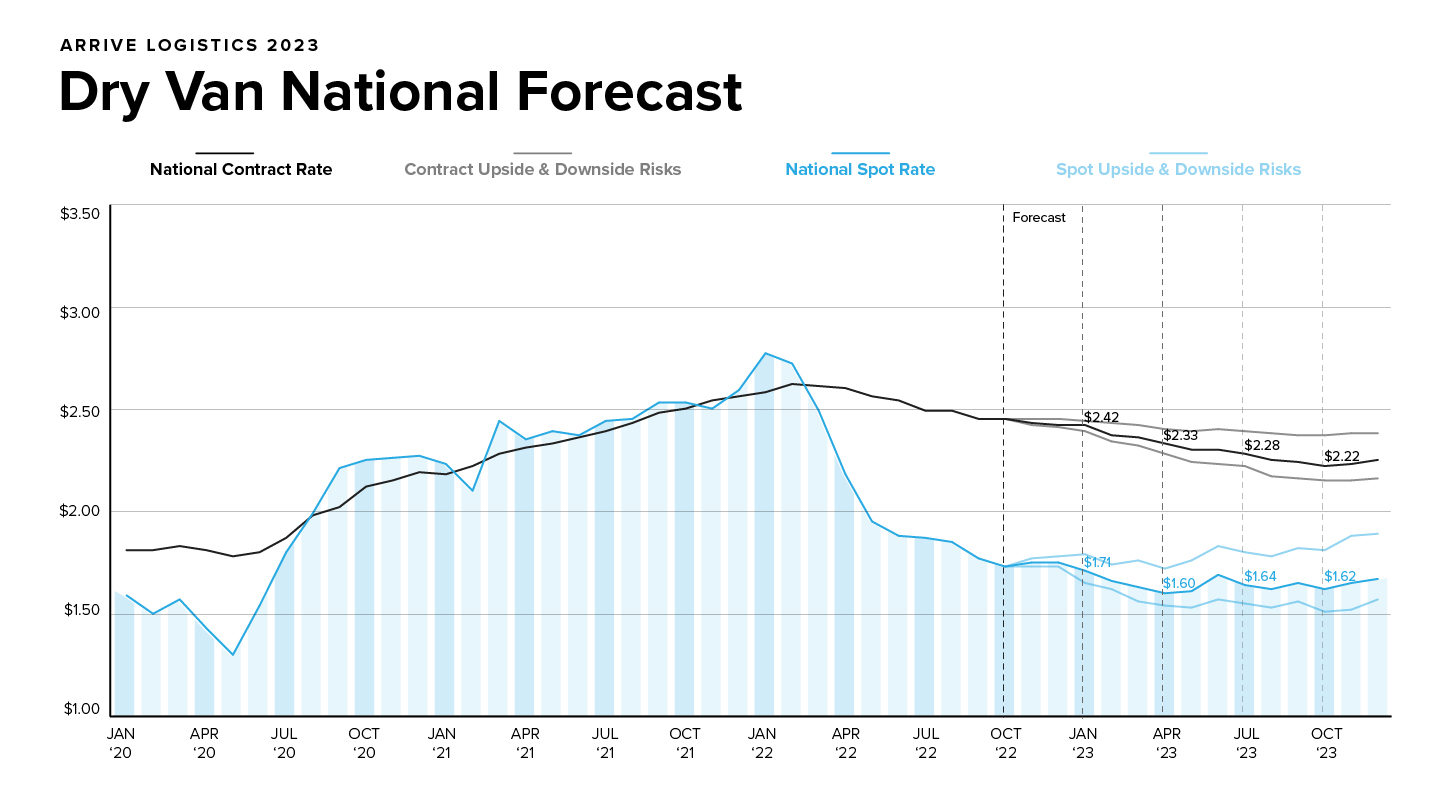

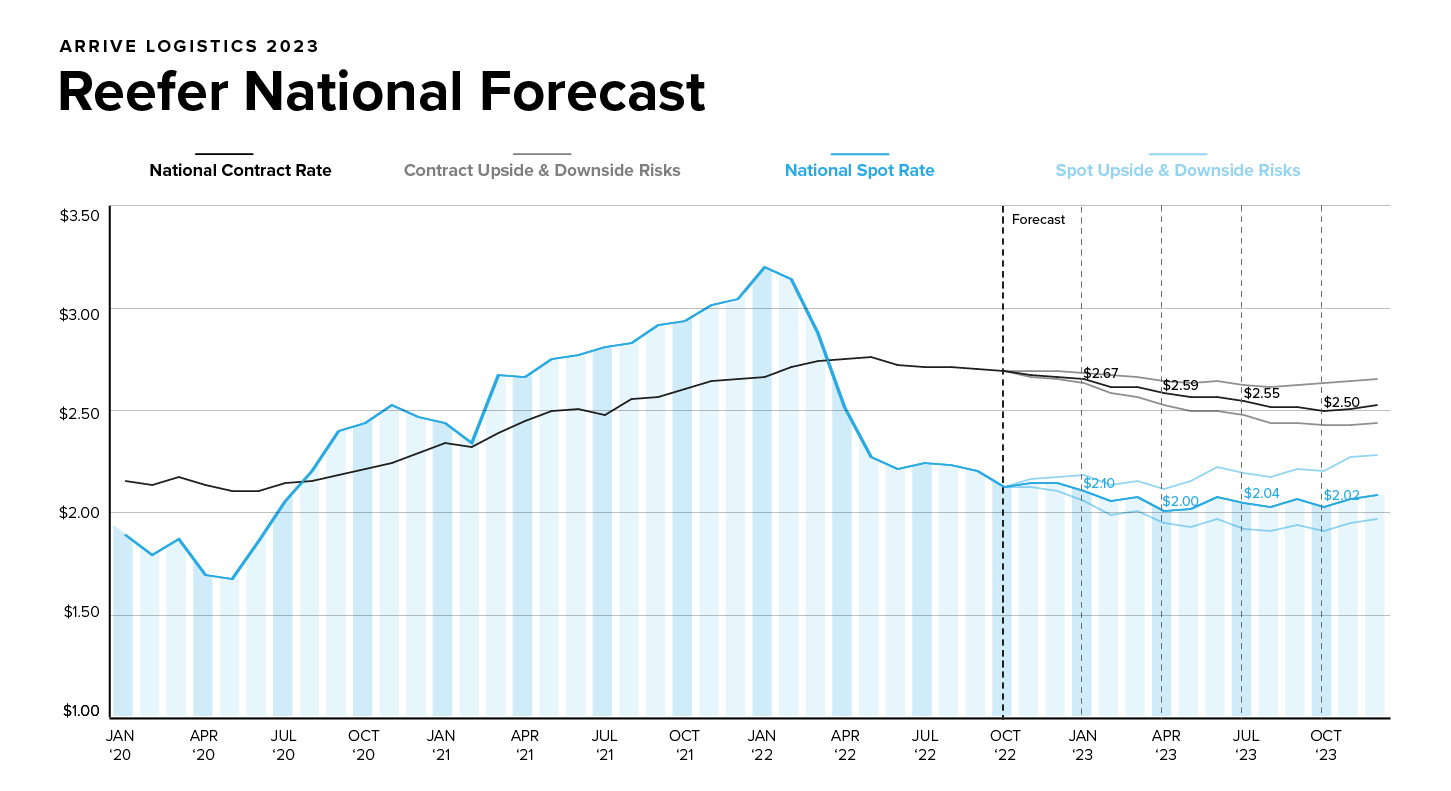

This document contains our comprehensive outlook for national dry van and reefer truckload rates for November 2022 through December 2023. The Arrive Insights® team generated this forecast through a combination of extensive historical research and output from the predictive models built into ARRIVEnow, our proprietary technology platform.

Successfully navigating freight market ebbs and flows begins with a basic understanding of the relationship between rates and the unique components of truckload supply and demand. Simply put, high or increasing demand and tight capacity will cause upward rate pressure, whereas low or easing demand and ample available capacity will drive rates down.

By tracking directional trends for truckload demand (volume) and available capacity (trucks) in the market at any given time, we can predict rate trends with a high degree of accuracy and consistency. With that, we present to you our rate forecast for the year ahead.

We expect spot rates to remain relatively stable as contract rates continue to normalize, gradually closing the gap between the two throughout the year. It is also likely that easing demand will outpace capacity exiting the market, at least in the short term, resulting in continued strong routing guide compliance. Finally, conditions in the first half of the year will continue driving significant capacity out of the market, making it more susceptible to disruptive events like widespread severe weather and unexpected demand surges.

Capacity will likely continue to be established on contractual freight as strong rates force more owner-operators and small fleets out of the market and into company jobs; healthy routing guide compliance is expected in turn. Further, significant capacity entered the market throughout the last inflationary rate cycle, driving total long-haul trucking employment to an all-time high. So, even as record numbers of carriers shut down, significant capacity remains as more drivers favor company jobs. That, plus the strong routing guide compliance seen through the summer peak season and fourth quarter onset, offers confidence that capacity can support current demand.

Overall freight tonnage declines are likely as economic conditions return to pre-pandemic levels. Still, truckload demand remains healthy compared to historical norms, though improved routing guide compliance has caused significant spot market demand declines. On the consumer front, inflation is leading to a decrease in spending, and rising interest rates are slowing the housing boom, which means fewer goods purchases and, in turn, decreased demand. That said, backlog fulfillment in manufacturing and industrial production will likely help prevent demand from falling off a cliff, supporting an outlook for more gradual easing.

This forecast shows what we believe will be the most likely scenario given current data and market conditions. However, the ongoing challenges listed below or other unexpected events may cause significant volatility.

The Russia/Ukraine conflict significantly impacted freight markets in 2022 and remains a concern heading into 2023. Similarly, tensions between China and Taiwan may impact Asia-U.S. relations and trade, including Taiwan’s prominent semiconductor production.

The tentative deal between rail carriers and rail employee unions has encountered some opposition, slowing the ratification process. While we believe it is unlikely, a strike could occur this quarter if either of the two largest unions votes to reject the agreement. The resulting demand shock would create a major disruption for over-the-road trucking.

We factored current economic conditions and a possible recession into our 2023 forecast. However, if conditions deteriorate faster than anticipated, falling consumer demand and pullbacks in manufacturing may result in decreased truckload demand.

Severe weather is a frequent source of freight market disruption. Though winter storms tend to have the greatest impact, healthy Q1 capacity should help mitigate any significant issues if major weather events occur.

Spot rates can only fall so far before carriers lose significant money and decide to pull trucks off the road or leave the market entirely. This floor means there is less room for spot rates to decline further, which is why our forecast displays less potential downside.

The national average spot rate per mile aggregates the weekly market-to-market, 7-day spot rates on lanes of 500 miles or more. The thresholds on market-to-market and 7-days help ensure we are using lanes of higher density, which are more representative of the true cost of most lanes. Additionally, the minimum threshold of 500 miles eliminates the inclusion of short hauls, which could inflate the index based on the rate per mile.

The national average contract rate per mile is sourced from DAT data and underwent no additional aggregation.